Global economic activity was mixed during the third quarter of 2023, with distinct signs of improvement in the United States and China but continued sluggishness elsewhere.

Global industrial production was up by just 0.4 percent in August 2023 compared with the same month a year earlier, according to estimates compiled by the Netherlands Bureau for Economic Policy Analysis (CPB).

But trade volumes were down by 3.8 percent in August compared with a year earlier and have not grown for a year, a sign of stagnation that is consistent with a recession (“World trade monitor”, CPB, Oct. 25). The United States and China, the world’s two largest economies, showed signs of growing somewhat faster in the third quarter after a pronounced slowdown in the first half of 2023.

Preliminary estimates show U.S. real gross domestic product increased at an annualised rate of 4.9 percent in the three months from July to September up from 2.1 percent in the three months from April to June. The largest contribution came from increased consumer spending (+2.7 percentage points) especially on services (+1.6 percentage points) with a smaller contribution from goods (+1.1 percentage points).

The acceleration is consistent with data from purchasing managers surveys showing service sector activity increased in the third quarter after the barest of slowdowns during the second quarter.

Manufacturing activity continued to decline but there were clear signs it was approaching a cyclical trough with expansion imminent.

CHARTBOOK: GLOBAL ECONOMY AND TRAD

Initial claims for unemployment benefits have trended lower since the start of July after rising throughout the first six months of the year.

Service sector prices rose at an annualised rate of 5.2 percent in the three months ending in September up from 3.3 percent in the three months ending in June.

But there were also warning signs that some of the strength may be temporary and not sustained in the coming quarters.

The second largest contributor to real gross domestic product growth in the third quarter came from business inventories (1.3 percentage points).

Contributions from inventory changes are normally reversed within 3-6 months so the tailwind in the third quarter is likely to turn into a headwind in the fourth.

Real final sales to private domestic purchasers (FSPDP), a measure that strips out volatile changes in inventories, trade and government spending, increased at an annualised rate of 3.3 percent between July and September.

Real final sales accelerated markedly from annualised growth of 1.7 percent between April and June and a contraction of -0.2 percent between October and December 2022. Final sales confirm the economy has returned to moderate growth after the briefest and shallowest of cyclical slowdowns at the end of 2022 and the start of 2023.

But there are questions about how sustainable the current rebound will prove.

There is not much spare capacity in the labour market or in energy supplies for renewed growth without sparking inflation.

The unemployment rate was just 3.8 percent in September while inventories of diesel and other distillate fuel oils were 19 million barrels (-15 percent or -1.29 standard deviations) below the prior 10-year seasonal average.

CHINA AND ASIA

China’s economy also appears to have returned to growth during the third quarter after a slump in the second quarter.

The manufacturing purchasing managers index improved for four consecutive months and by September was in the 38th percentile for all months since 2011 up from just the 2nd percentile in May.

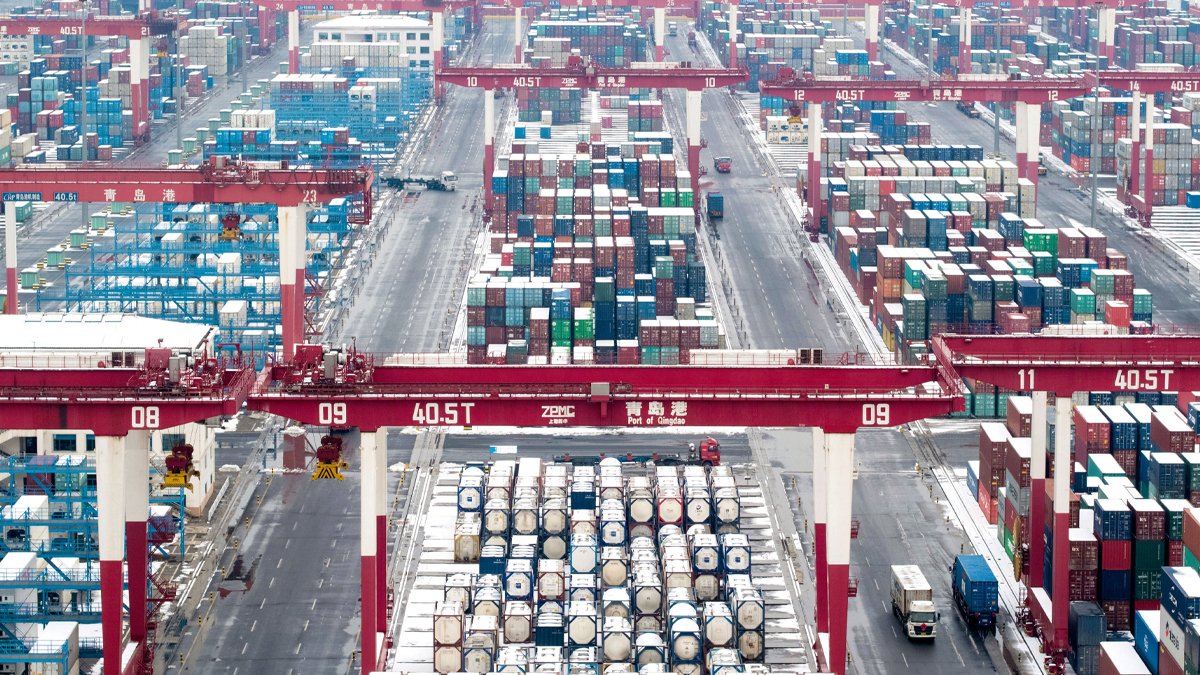

The volume of containers handled by China’s coastal ports was up almost 8 percent in September compared with the same month a year before, according to data from the Ministry of Transport.

China’s electricity generation was up 9 percent in September compared with a year earlier, with big increases in power consumed by service sector firms (17 percent), manufacturers (9 percent) and primary industries (9 percent).

China’s recovery is helping lift other regional economies. Singapore acts as a major transshipment hub for trade between Asia and Europe and freight volumes also show signs of accelerating.

The port handled a record volume of shipping containers in the last 12 months and volumes were up more than 4 percent in September compared with a year earlier.

But in Japan, the volume of air cargo remains in the doldrums, with freight through Narita International Airport down by 23 percent compared with a year ago and showing no sign of recovering.

South Korea’s KOSPI-100 equity index, which is usually a good proxy for global trade given its heavy weighting towards export-oriented firms, rebounded strongly through the end of July.

But the index has since weakened, consistent with the renewed downturn in volumes shown in the global trade index.

Global container shipping rates have fallen again in both September and October after rising over the summer in another sign demand remains sluggish.

Europe remains the weakest region as it struggles with the combined impact of higher energy prices and the disruption of trade flows following Russia’s invasion of Ukraine as well as persistent inflation and higher interest rates.

In Germany, energy-intensive manufacturers reported output was still down by down 16 percent in August 2023 compared with January 2022 before Russia’s invasion and shows no sign of recovering